Export supplies to third countries are exempted from VAT in Belgium and throughout the EU. However, to benefit from the VAT exemption, the supplier is required to prove that the goods have left the EU. In Belgium, the export customs declaration (Single Administrative Document - SAD) is the most important document for establishing such a proof for claiming the VAT exemption. Traditionally, the Belgian VAT authorities have required that suppliers claiming the VAT exemption are to be named as the exporters of record in Box 2 of the SAD.

The new UCC now applies a new definition concerning the exporter of record. This is the party that has the power to determine that the goods are shipped outside the EU. Furthermore, the new definition indicates that the exporter of record should be established in the EU. If a non-EU company has the power to determine that the goods are shipped outside, then it will need to appoint an indirect customs representative established in the EU that should act as the exporter of record. The exporter of record must be stated in Box 2 of the SAD.

However, the UCC provides for a transitional period, during which the non-EU established company may continue to be named in Box 2 of the SAD. This transitional period will end in 2019 with the introduction of the Automated Export System (‘AES’).

For VAT purposes, the VAT exemption is linked to the person who supplies the goods and invokes the VAT exemption for export. Taking into account the new definition of exporter for customs purposes, the exporter of record named in Box 2 of the SAD will, in a number of cases, not necessarily be the person claiming the VAT exemption for export.

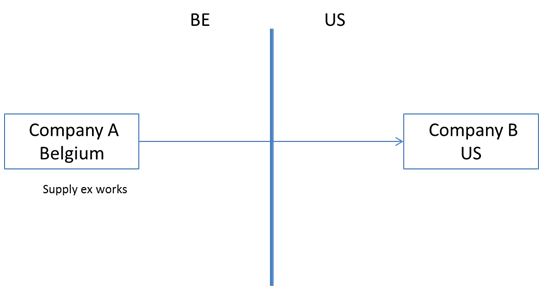

A good example to illustrate this change is the situation of an EU company that is supplying goods for export to a non-EU company under the incoterm “ex works”. As the non-EU company is responsible for the export of the goods outside the EU, this company will be the exporter for customs purposes. In any case, it will need to appoint an indirect customs representative for handling the customs declaration for export. Currently, this requirement means that the non-EU company is named in Box 2 of the SAD, while the indirect customs representative is named in Box 14 of the SAD. However, the EU supplier will invoke the VAT exemption for export. As this EU supplier is not named as the exporter in the SAD, there is an issue of proving the exemption from a Belgian point of view.

The Belgian tax authorities have decided to solve this issue by making a distinction in the SAD between the exporter of record for customs purposes (based on the UCC definition) and the exporter for VAT purposes (the company claiming the VAT exemption). Since 1 May 2016, the exporter for VAT purposes must be named in Box 44 (name and VAT number), whereas the exporter for customs purposes must be stated in Box 2 of the SAD.

It is important to note that this rule also applies where the exporter for customs is also the person claiming the VAT exemption for export.

Currently, the new rules can be illustrated as follows:

The SAD should state the following:

- Box 2: company B as the exporter for customs;

- Box 14: EU Indirect representative for customs; and

- Box 44: company A as the exporter for VAT.

This is a practical solution from a Belgian perspective. It is very important for companies involved in export transactions to strictly comply with these new rules, particularly regarding the references in Box 44 for the VAT exemption.

Please note that the application of these new rules is not always that clear in complex chain transactions or transactions involving the processing/assembling of goods before export. Furthermore, other EU Member States can follow other rules for customs compliance and for proving the VAT exemption. Companies with export transactions in various EU member states should make sure that they comply with all the applicable rules.

Monday, 27 June 2016

Impact of the new customs rules on the VAT exemption for export

Since 1 May 2016, the Union Customs Code (the UCC) has entered into force in the European Union. The UCC modernises customs law and serves as the new framework regulation on the rules and procedures for customs throughout the EU. Although the UCC does not directly alter the VAT Directive (2006/112/ZG) or any other VAT rules, it has an indirect impact on the VAT exemption for export supplies. Recently, the Belgian authorities have published practical guidelines on this issue (see VAT Decision no. 129.169 of 20 May 2016).